A qualified defined benefit plan, sometimes known as a Pension Plan, presents a frequently overlooked tax advantage for businesses and/or business proprietors. Businesses eligible for this plan include:

- Sole proprietors

- C-Corporations

- S-Corporations

- Partnerships

- Limited Liability Companies

- Family Limited Partnerships

This plan primarily caters to pass-through entities, hence it's less common to see them utilized by C-Corps. Although smaller businesses are the usual beneficiaries, larger enterprises can also avail themselves of its benefits.

These plans allow for the most substantial tax-deductible contribution to a qualified retirement plan. In many instances, this can result in a six-figure tax deduction for a business and/or individual. There have even been instances where it facilitated deductions in the seven figures.

Typically, the older the individual, the greater the contribution they can make under this plan. This is because the benefit is predetermined, not the contribution. Thus, older individuals can contribute more to "catch up" to the maximum defined benefit.

Moreover, the Tax Cuts and Jobs Act (TCJA) permits pairing this plan with IRC section 199A, allowing eligible taxpayers a deduction of up to 20 percent of qualified business income (QBI) under certain eligible business entities and industries.

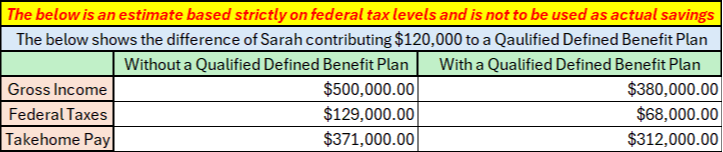

The below is an estimate based strictly on federal tax levels and is not to be used as actual savings, consult with your own tax professional before making any decisions

Consider the case of Sarah, a fictional sole proprietor who discovered the immense potential of a certified defined benefit plan. After all of Sarah's Qualified Business Expenses (QBE) her QBI is $500,000. At this rate, Sarah would pay about $129,000 in taxes bringing her net, or "take-home" pay to $371,000.

If Sara contributes $120,000 to a Qualified Defined Benefit Plan, this would bring her under the IRC Section 199A threshold, which would give her an additional 20 percent deduction on her QBI. See the below example:

In this hypothetical instance, the "net" cost for Sarah to contribute $120,000 to a qualified retirement plan is $59,000. So instead of paying Uncle Sam six figures in taxes, she has paid herself $120,000, and allowed Uncle Sam to "subsidize" her retirement.

Just like Sarah, business owners across the country are unlocking the full potential of certified defined benefit plans to secure their financial future and minimize their tax liabilities. With the right guidance and expertise, you too can harness the power of these innovative solutions to achieve your retirement goals. Don't let tax season be a source of stress – explore the possibilities of certified defined benefit plans today and pave the way for a brighter tomorrow.

To summarize the key advantages:

- A certified defined benefit plan offers substantial retirement benefits devoid of market risk.

- It provides the largest tax deduction under the law from a retirement perspective.

- It can furnish guaranteed income that one cannot outlive.

- It mitigates, diversifies, or eliminates market risk.

- It enables the purchase of estate planning tools on a pre-tax basis.

- There is no full-funding limitation under IRC Section 404(a)(1)(A).Quarterly contributions are not mandatory.

- Under-funding is not possible because contributions are based on the guaranteed provisions of the level premium contracts.

Despite these advantages, there are some drawbacks to consider:

- It necessitates contributions to be made annually for at least five years.

- Policy loans are not available.

- There's limited flexibility in contribution allocations.

- Investment allocations within the plan may be restricted.

However, there's still an opportunity to implement this plan for a 2023 deduction but you will need to file an extension.

Jesse Somdahl is the Director of Operations at Finance For Thought and can be reached through our office on our website.

Disclosures:

TAX- To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purposes of avoiding penalties that may be imposed by law. Each tax payer should seek tax, legal or accounting advice from a tax professional based on his/her individual circumstances.

TAXES- This material is for informational purposes only. Neither Finance For Thought, FFT nor its Representatives provide tax, legal or accounting advice. Please consult your own tax, legal or accounting professional before making any decisions.

Sources:

https://www.irs.gov/newsroom/tax-cuts-and-jobs-act-a-comparison-for-businesses

https://www.irs.gov/retirement-plans/choosing-a-retirement-plan-defined-benefit-plan

https://www.irs.gov/retirement-plans/defined-benefit-plan

https://www.planadviser.com/412e3-plans-for-small-business-clients/

https://www.irs.gov/businesses/small-businesses-self-employed/deducting-business-expenses